Multicategory recall highlights the cost of poor warehouse controls

In December 2025, a large multicategory recall was triggered after the U.S Food and Drug Administration (FDA) found unsanitary conditions at a wholesale facility in Minneapolis. Specifically, Gold Star Distribution Inc., a north Minneapolis distributor, was found to be storing products in areas contaminated with rodent urine, rodent feces, and bird droppings. Since the company handled a broad range of FDA-regulated products, the recall encompassed numerous categories, including food items, over-the-counter medications, cosmetics, medical products, dietary supplements, and pet items.

According to the FDA, products stored in such unsanitary conditions may have been contaminated with harmful microbes, posing serious health risks to consumers.

This included a risk of exposure to Salmonella, which can cause gastrointestinal illness, and Leptospira, which can lead to leptospirosis, an infection that causes flu-like symptoms. Both illnesses can be dangerous or even fatal, especially in vulnerable groups such as older adults, pregnant individuals, and people with weakened immune systems. Furthermore, contaminated cosmetics may have caused irritation or adverse reactions, while contaminated medical devices may have increased the risk of infections among consumers.

The FDA marked the recall as Class II, meaning the products posed a risk of temporary or medically reversible health effects, though the likelihood of serious health consequences was considered remote. Consumers and retailers were instructed to destroy the items and to contact Gold Star for a refund.

Why this case matters

The Gold Star recall demonstrates how a single point of failure anywhere in the supply chain—in this case, inadequate warehouse sanitation—can affect multiple products, brands, and industries at once. Rather than a single defective product, nearly 2,000 products were compromised across multiple categories, and several high-profile brands were affected by the recall, including Coca-Cola, Hershey’s, and Tylenol. The recall also impacted more than 50 retail locations across Indiana, Minnesota, and North Dakota, which had to remove inventory and follow destruction or return protocols.

Additionally, the case underscores the significant risks associated with third-party providers, since even manufacturers with safe production practices had to recall products because they relied on Gold Star for storage. It also highlights that when multiple products and brands are involved, managing consumer communications, retailer coordination, logistics, and regulatory notifications becomes significantly more complex.

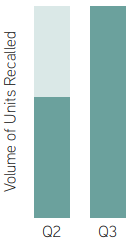

The number of FDA recall events rose 1.4% between the second and third quarters of 2025, reaching 145, the second-highest quarterly total for FDA food recalls since the first quarter of 2020, according to analysis of U.S. product recall data by Sedgwick Brand Protection. Moreover, the volume of units recalled increased by 75.8% in Q3 2025, indicating that recall events grew larger and involved far more products per event.

Who is impacted in a situation like this?

Numerous parties are impacted in cases involving widespread recalls linked to third-party storage conditions, including the following:

- Distributor/warehouse operators are exposed to regulatory scrutiny, financial losses, and reputational damage when storage conditions fail to meet sanitary or compliance standards.

- Manufacturers and brand owners face inventory losses and customer trust challenges as products bearing their brands are withdrawn from sale because of third-party contamination, even when manufacturing practices were sound.

- Retailers are required to remove impacted inventory from shelves, follow destruction procedures, and manage customer inquiries and refund requests.

- Consumers (and pet owners) are exposed to potentially harmful organisms (e.g., Salmonella) that could cause health concerns or harm pets. They also lose trust in brands and products, as they experience inconvenience and uncertainty about which items are safe.

- Regulators are tasked with overseeing the recall and ensuring harmful products are removed effectively to protect public safety, as well as conducting follow-up inspections, imposing enforcement actions, and requiring corrective measures.

How this case fits into overall recall trends

The Gold Star recall demonstrates that recalls can result from control failures, not just product defects. Consider the following common recall drivers among many recall cases:

- Undeclared allergens—Mislabeling, cross-contamination during manufacturing processes, or a supplier’s failure to disclose ingredients can result in products containing undeclared allergens, leading to recall action.

- Bacterial contamination—Environmental monitoring failures or poor sanitation can allow harmful bacteria to enter the production environment, contaminate surfaces or equipment, and migrate into finished products, prompting recalls.

- Foreign materials—Inadequate equipment maintenance or human errors (e.g., an employee dropping jewelry into a production line) can lead to physical items getting into products, triggering recalls.

In the case of the Gold Star recall, the cause was unsanitary storage conditions and poor handling practices that posed a contamination risk.

Ultimately, problems don’t just occur at manufacturing plants—they can arise anywhere along the supply chain. As such, businesses must maintain strong controls throughout manufacturing, storage, transportation, and retail handling.

Why product recall insurance matters

Product recalls can lead to significant financial losses for affected businesses. These losses often include both direct costs (e.g., retrieving products, handling logistics, and managing disposal) and indirect costs (e.g., lost sales, reputational damage), which together can lead to financial strain or even bankruptcy.

Product recall insurance can reduce this financial exposure by covering a range of recall-related expenses, which may include the following:

- Notifying customers, retailers, and regulators—These associated costs involve formally notifying all affected parties, including mandatory notifications to regulatory bodies such as the FDA. Coverage may also include costs for extra staff to handle customer and retailer inquiries.

- Shipping, handling, and storing returned goods—These are costs involved with retrieving recalled products from retailers or distributors, transporting them to destruction sites, and documenting the chain of custody.

- Inspecting, sorting, and destroying products—These expenses are the costs of inspecting returned items, conducting microbial and chemical testing, determining salvageability, and disposing of affected products.

- Replacing products (depending on policy)—This expense is associated with producing and distributing replacement inventory when products are withdrawn from the market.

Some policies may also include crisis management or brand recovery support to restore a company’s image and public perception.

{{richtext-cta-general-1="/components/rich-text-cta"}}

It’s worth noting that product recall insurance does not include coverage for lawsuits stemming from recall events. This is where product liability insurance comes in. Product liability coverage is designed to cover claims alleging that a defective or contaminated product caused bodily injury or property damage. That said, this coverage type does not help with the operational costs of the recall itself, which were significant in the case of the Gold Star incident. As such, carrying both product recall insurance and product liability coverage may offer the strongest financial protection.

Risk management lessons for businesses

To reduce their exposure to recall events, businesses should consider the following risk management lessons:

- The need for robust oversight of third-party warehouses—Businesses should rigorously vet suppliers and manufacturers to ensure compliance with safety standards and to set contractual expectations for sanitation, pest control, temperature control, and other critical safeguards. They should maintain oversight through routine audits and unannounced inspections, requiring warehouses to maintain strong documentation and implement corrective action processes to address any issues identified.

- The importance of being ready for a recall event—Businesses should keep a written plan detailing the process they will follow when executing a recall, including how they will identify affected lots, stop distribution, notify affected parties, and retrieve and dispose of faulty or contaminated products. It’s essential to map distributors and maintain accurate shipment records and lot codes, as well as assign roles for decision-making and communication during recall events.

- The role of preventive controls in reducing recall risk—Businesses should develop robust control measures to minimize harm from recall event drivers. In particular, controlling recipe changes, cleaning production lines so allergen-containing materials aren’t introduced to new products, and implementing strict label checks can reduce the likelihood of undeclared allergen recalls; executing strong sanitation and environmental practices can reduce the likelihood of bacterial contamination; and using metal detectors and X-ray scanning alongside routine equipment maintenance can minimize the likelihood of recalls due to foreign materials.

- The critical nature of retail and distribution preparedness—Retailers and distributors must be ready to halt sales and distribution immediately when a recall is announced. Their plans should include stop-sale procedures, processes for removing and documenting returned products, and clear customer service and refund protocols.

Strategic takeaways for risk and business leaders

The Gold Star recall event underscored several strategic takeaways as follows:

- Supply chain partners create shared risk. Even manufacturers with strong risk management practices can suffer recalls if their distributor or storage partner fails in their duties. Businesses should assess where supply chain failures can occur and put controls in place to minimize their exposure.

- Regulatory issues become brand and financial issues. Businesses with no operational fault may still face lost sales and reputational damage if the FDA or another regulatory body issues a recall due to failures elsewhere in the supply chain. Businesses should review the regulatory standards for their industry and consider both upstream and downstream impacts of recall events.

- Recalls are business continuity events. Just like other crisis events (e.g., natural disasters or system outages), major recall events can threaten a company’s ability to operate and cause widespread losses, including lost revenue, legal exposure, and reputational damage. Businesses must have a written recall response plan so they can respond quickly and effectively.

- Resilience requires both controls and insurance. Robust risk controls are essential to minimize the likelihood of recall events, yet certain failures—especially those in third-party environments— may fall outside a company’s direct control. As such, product recall insurance serves as a valuable risk management tool to lessen potential financial exposure.

Conclusion

As evidenced by the Gold Star Distribution Inc. recall event, recalls don’t always stem from product defects. A failure anywhere along the supply chain can have cascading effects, leading to product withdrawals across multiple categories, brands, and industries.

Businesses should review their exposure to control failures, both in-house and via third parties, to identify where and how recall events could occur to guide robust risk mitigation measures. Companies should also review both product recall and product liability coverage, which can provide much-needed financial protection for associated losses in these types of recall events.

Contact us today for more risk management and coverage solutions.

Provided by Christensen Group Insurance. This document is not intended to be exhaustive, nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel or an insurance professional for appropriate advice. © 2026 Zywave, Inc. All rights reserved.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

%20(1).webp)