Micah Salas brings over a decade of experience in the insurance industry to his role. He has experience in multiple industries, with a specialized focus in heavy civil and site construction. Micah holds a bachelor's degree in Business Administration with a marketing focus from the University of Wisconsin-Whitewater and has earned his Certified Insurance Counselor (CIC) designation.

{{cta-contact-popup="/components/rich-text-cta"}}

If your business owns vehicles, sends employees to job sites, delivers products, or operates a fleet of any kind, you may be asking the same question as many other business owners: why is my commercial auto insurance going up?

Unfortunately, the answer isn’t tied to a single factor. Rising commercial auto insurance rates are being driven by higher claim costs, more expensive repairs, distracted driving, attorney involvement, medical inflation, and larger jury awards. Even as some areas of the commercial insurance market have stabilized, commercial auto remains one of the most challenging lines of coverage for many businesses.

For small and mid-sized businesses, the issue is especially important. A company doesn’t need a large fleet to face serious auto-related risk. A single van, pickup, box truck, or employee-driven vehicle can create liability exposure if an accident leads to injuries, litigation, or a disputed claim.

The good news is that businesses are NOT powerless.

While you may not be able to control the broader insurance market, you can control how your company hires drivers, manages vehicle use, monitors behavior, responds to incidents, and documents safety practices.

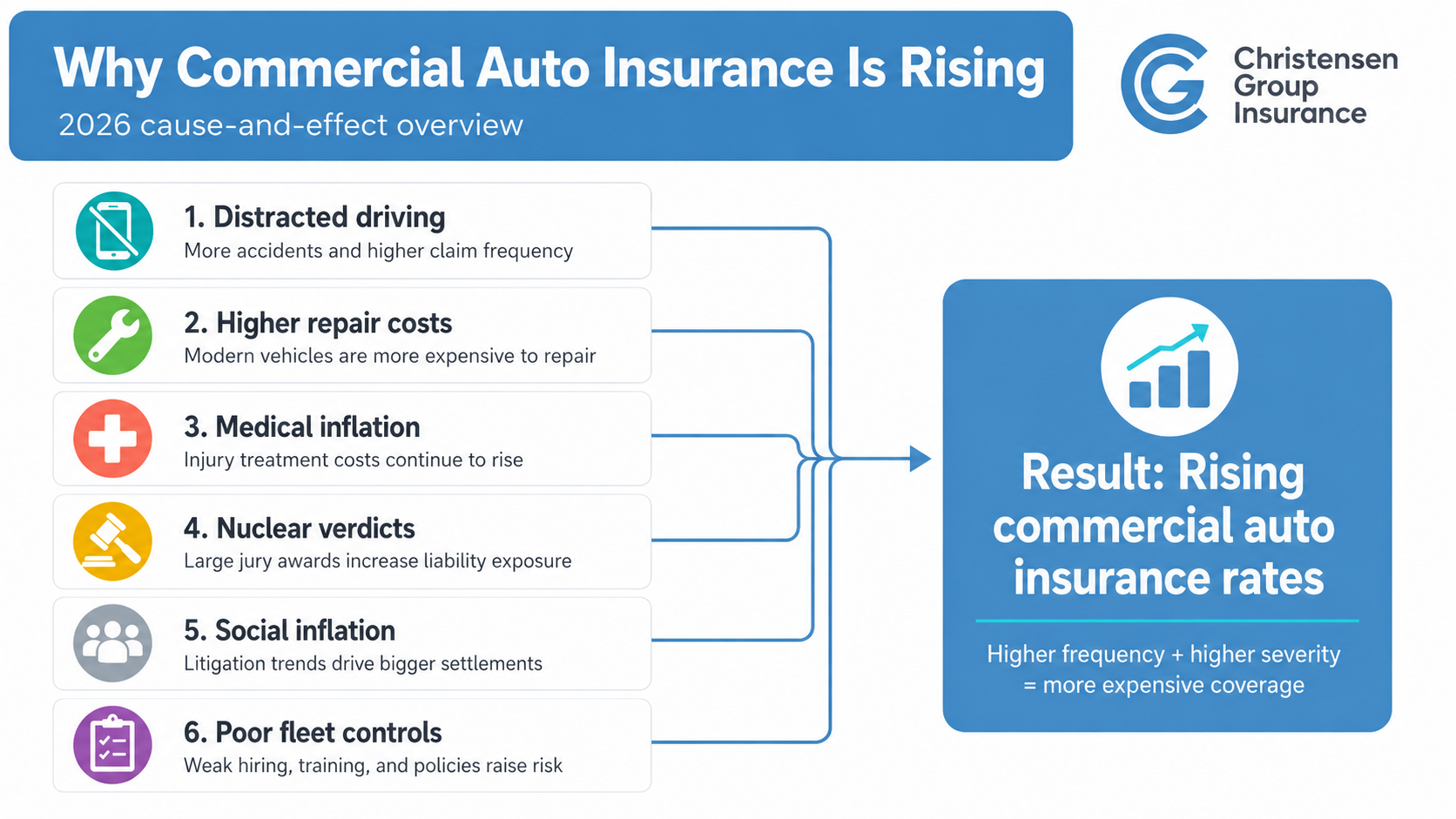

Why are commercial auto insurance rates rising in 2026?

The short answer is that commercial auto claims are becoming more expensive.

Vehicle repairs cost more than they used to because cars, trucks, and commercial vehicles now contain more sensors, cameras, electronics, and specialized parts. A minor collision that once required a bumper repair may now involve recalibrating driver-assistance systems or replacing technology built into the vehicle.

Medical costs are also higher. When an accident involves bodily injury, expenses can escalate quickly through emergency care, follow-up treatment, rehabilitation, and legal involvement.

At the same time, distracted driving continues to increase claim frequency. Phone use, GPS adjustments, eating, fatigue, and multitasking behind the wheel can all contribute to preventable accidents. For businesses, even small crashes matter because a pattern of frequent claims can affect how carriers view the account.

Another major factor is claim severity. Commercial auto accidents can involve larger vehicles, work-related travel, cargo, equipment, employees, customers, and members of the public. When a claim turns serious, the financial consequences can extend far beyond the initial damage.

Underneath these rising claim costs is a broader market cycle. Commercial auto has been a hard market for years, meaning carriers have tightened underwriting and pushed rates up to restore profitability after a long stretch of underwriting losses. Insurers track this through the combined ratio, which measures incurred losses, loss-adjustment expenses, and underwriting expenses as a percentage of earned premium. A ratio above 100% signals an underwriting loss.

Commercial auto has operated above breakeven in most years since 2011, with only brief improvement during the pandemic period. Recent results show the line is still under pressure: commercial auto posted a 107.2% combined ratio in 2024, while commercial auto liability was even higher at 113.0%. S&P Global projects commercial auto combined ratios will remain above 100% through at least 2029. Litigation pressure is another reason loss costs remain elevated. Corporate nuclear verdicts over $10 million increased 52% from 2023 to 2024. Until carriers see loss costs improve, upward rate pressure is likely to continue.

How much have commercial auto insurance rates increased?

Some businesses may see modest increases, while others may face larger jumps, especially if they have prior claims, poor driver controls, heavy vehicles, long-distance operations, or higher-hazard routes.

Rate changes vary by:

- Business

- Industry

- State

- Fleet size

- Vehicle type

- Loss history

- Coverage structure

Recent market reports continue to show commercial auto rates increasing even as other commercial insurance lines have softened. One industry benchmark showed commercial auto marking another consecutive quarter of increases in late 2025, with average increases in the mid-single digits.

Over a longer horizon, the climb is steeper. According to the Federal Reserve Bank of St. Louis’s Producer Price Index, U.S. commercial auto insurance premiums rose more than 19% from mid-2015 to mid-2025, and roughly 6.7% over the most recent year, outpacing the roughly 2.7% increase in the Consumer Price Index over the same period.

However, averages only tell part of the story. A business with clean losses, strong driver screening, telematics, documented maintenance, and clear vehicle-use policies may have a better renewal conversation than a business that can’t show how it manages fleet risk.

That’s why the most important question isn’t “why is commercial auto insurance rising?” It’s “what can we show underwriters about how we control risk?”

What is a nuclear verdict, and why does it affect commercial auto insurance?

A nuclear verdict is generally understood as an exceptionally large jury award, often $10 million or more. These verdicts can arise from serious injury or fatality claims, including commercial auto accidents.

Even if your business has never had a major claim, nuclear verdicts can affect your insurance costs because insurers price coverage based on the possibility of severe losses across the market. When verdicts and settlements rise, carriers become more cautious. They may increase rates, reduce appetite for certain risks, require higher limits, scrutinize driver records more closely, or ask more detailed questions about safety controls.

This trend is known as “social inflation,” which refers to the rising cost of insurance claims due to factors beyond ordinary economic inflation. These factors may include litigation trends, broader jury awards, attorney advertising, third-party litigation funding, and greater skepticism toward corporate defendants.

For business owners, the practical takeaway is simple: even a “small” accident can become a much larger financial problem if injuries, disputes, documentation gaps, or poor driver history are involved.

If you’re curious about how one of these can play out, we recently documented a $15.8 million nuclear verdict involving Topgolf.

Why small fender benders can become big claims

Many businesses think of commercial auto risk in terms of major crashes. But small incidents can also create big problems.

A minor rear-end accident may lead to injury allegations. A low-speed parking lot collision may involve a pedestrian. A driver using a personal vehicle for work may create coverage questions. A claim that was not reported promptly may become harder to defend. A missing maintenance record or incomplete driver file may make the business look less prepared than it actually is.

Commercial auto claims become more difficult when businesses do not have clear policies or documentation. If an insurer, attorney, or claimant asks what your company does to prevent accidents, you want to have a strong answer.

That answer should include driver hiring standards, safety training, vehicle maintenance, incident reporting procedures, and technology where appropriate.

How to lower commercial auto insurance premiums

There’s no single way to guarantee lower premiums, but businesses can improve their risk profile by showing carriers that fleet safety is actively managed. Here are five strategies to consider.

- Hire and retain qualified drivers

Driver quality is one of the most important factors in commercial auto performance. Businesses should have a consistent process for reviewing motor vehicle records, verifying licenses, evaluating experience, and setting standards for acceptable driving history.

Driver screening shouldn’t stop at hiring, either. Motor vehicle records should be reviewed regularly, and businesses should have a process for addressing violations, accidents, and other unsafe behavior.

{{richtext-cta-business-insurance="/components/rich-text-cta"}}

- Create clear vehicle-use policies

A written vehicle-use policy helps establish expectations before an incident occurs. It should address who is allowed to drive, when company vehicles may be used, whether personal use is permitted, how mobile devices should be handled, and what drivers must do after an accident.

For companies with employees who use personal vehicles for work, the policy should also address proof of personal auto insurance and when business use is permitted.

Also read: Why are personal auto insurance rates rising?

- Train drivers on real-world risks

Driver training should go beyond basic orientation. Businesses should reinforce safe following distances, distracted driving prevention, backing procedures, speed management, defensive driving, weather-related risks, and accident response.

Training is especially important for businesses with changing routes, seasonal employees, younger drivers, delivery operations, or job-site exposures.

- Maintain vehicles consistently

Preventive maintenance can help reduce breakdowns, unsafe conditions, and post-accident scrutiny. Businesses should keep records of inspections, repairs, tire maintenance, brake service, and scheduled maintenance.

Strong maintenance documentation can also help show underwriters that vehicles are being managed responsibly.

- Review claims and near misses

Businesses shouldn’t wait for renewal to evaluate fleet performance. Reviewing accidents, near misses, citations, and driver behavior throughout the year can help identify patterns before they lead to larger losses.

For example, frequent backing incidents may signal the need for additional training, mirrors, cameras, spotter procedures, or route adjustments.

Do telematics and dashcams really reduce commercial auto insurance costs?

Telematics and dashcams can be valuable, but they should be viewed as risk management tools first and discount tools second.

Telematics can help businesses monitor speeding, harsh braking, rapid acceleration, mileage, route patterns, and driver behavior. Dashcams can provide helpful context after an accident, especially when liability is disputed.

These tools may help improve underwriting conversations because they show that the business is monitoring and addressing unsafe behavior. In some cases, they may also help reduce claim costs by providing evidence quickly after an incident.

However, technology only works when businesses use the data. Installing telematics but never reviewing reports is unlikely to change driver behavior. The strongest programs combine technology with coaching, accountability, and consistent follow-up.

Should small businesses with only a few vehicles worry about rising rates?

Yes. Small businesses with only a few vehicles should still take commercial auto risk seriously.

A company doesn’t need a large fleet to experience a costly claim. One employee running errands, delivering materials, visiting clients, or driving between job sites can create exposure. For contractors, service businesses, distributors, landscapers, manufacturers, and professional service firms, vehicles are often essential to daily operations.

Smaller businesses may also have fewer financial resources to absorb a large deductible, uninsured loss, downtime, or legal dispute. That makes proper coverage and risk management even more important.

If your company uses trucks, trailers, or heavy equipment, it may also need specialized coverage considerations. Christensen Group provides insurance solutions for trucks, trailers, and heavy equipment to help businesses address these exposures more effectively.

What businesses should review before renewal

Before your next commercial auto renewal, consider reviewing the following:

- Driver qualification files and motor vehicle record checks

- Written vehicle-use and distracted driving policies

- Accident reporting procedures

- Maintenance and inspection records

- Telematics or dashcam data

- Claims history and loss trends

- Employee use of personal vehicles for business

- Coverage limits, deductibles, and endorsements

- Hired and non-owned auto exposures

- Umbrella or excess liability limits

This review can help identify gaps before an underwriter does. It can also create a stronger renewal story, especially if your business has made improvements since the last policy period.

For a broader overview of protection, read our article on the benefits of commercial auto insurance.

Build a stronger commercial auto risk strategy

The commercial auto insurance market outlook for 2026 remains challenging, but businesses can take meaningful steps to manage their risk. Rates may continue to rise for many companies, especially those with poor losses, weak controls, or limited documentation. But businesses that invest in driver quality, safety practices, technology, and policy structure may be better positioned.

At Christensen Group, we help businesses understand why their commercial auto insurance is rising, identify the factors driving their renewal, and build a plan to reduce risk over time.

Our team can help you review your fleet exposures, evaluate coverage options, strengthen safety practices, and align your commercial auto program with your broader business insurance solutions.

If rising commercial auto insurance rates are putting pressure on your business, now is the time to take a closer look. Contact Christensen Group today to discuss your commercial auto coverage, fleet safety strategy, and opportunities to improve your risk profile before your next renewal.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

%20(1).webp)