Through extensive experience in his previous role as an underwriter, Zach has specialties across the liability spectrum. His primary focus at Christensen Group spans Management Liability (Directors & Officers/Employment Practices/Fiduciary/Crime), Cyber Liability, Professional Liability/Errors & Omissions, Social Services/Non-Profit Organizations, Habitational/Multi-Family Housing, and Restaurant/Retail industries.

When small business owners search for the cost of cyber insurance, they usually want one clean number. But the honest answer is that there is no universal 2026 rate card.

A small professional services firm with limited sensitive data, strong controls, and a modest limit can price very differently from a healthcare practice, retailer, manufacturer, or technology company with more records, vendors, endpoints, and privacy exposure. Carriers look closely at the details of your risk before they ever price coverage.

For this article, “small business” generally refers to organizations with roughly 1 to 100 employees and annual revenue under $10 million, though some insurers may classify businesses differently based on industry, operations, and risk profile. This may include professional services firms, contractors, manufacturers, retailers, and other privately held businesses that have less complex technology environments than large enterprise companies but still face meaningful cyber risk.

What is the average cyber insurance cost for a small business in 2026?

The good news is that, in 2026, cyber insurance remains a favorable market for many buyers. There is plenty of capacity in the marketplace, and carriers continue to broaden coverage and increase sub-limits for well-controlled risks. Despite rising claim activity, many insureds are seeing flat to slightly lower pricing on an apples-to-apples basis.

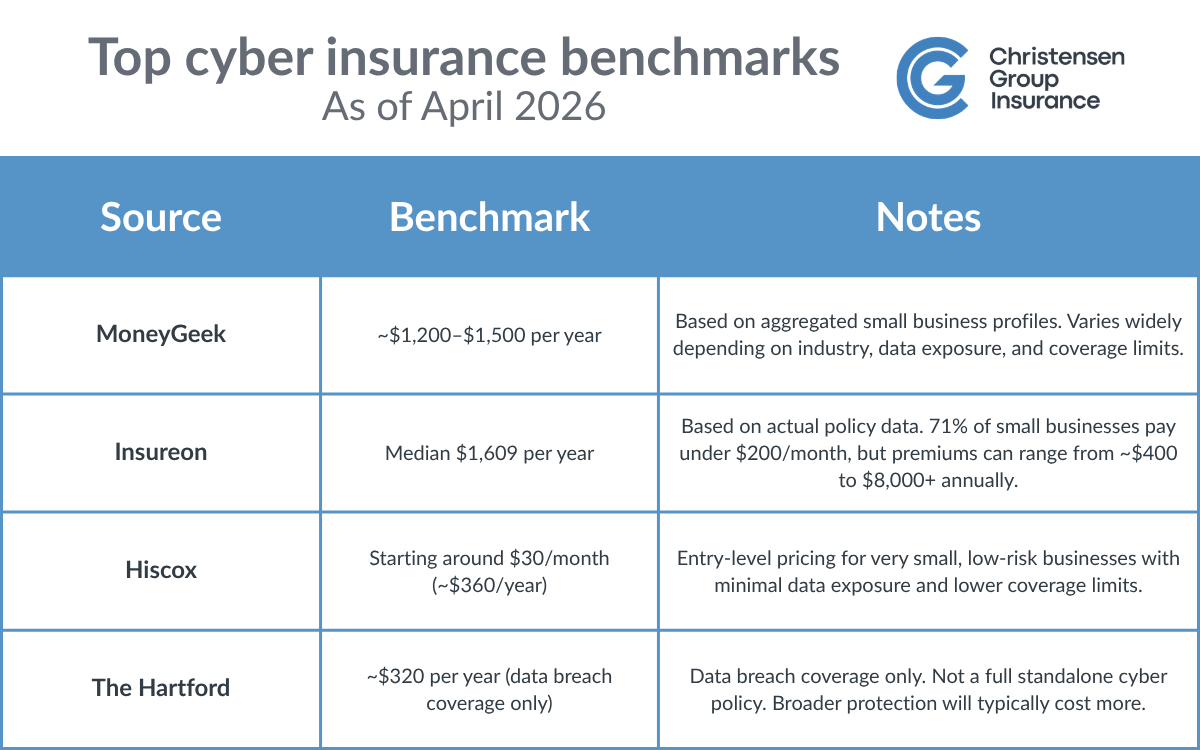

For many small businesses, standalone cyber coverage with a $1 million limit typically starts around $1,500 annually, though actual quotes may be higher or lower depending on the risk.

Note: That is only an estimate, not a quote.

Public benchmarks can provide helpful context, but they do not always compare the same type of coverage. Some pricing reflects limited data breach endorsements, while other pricing reflects broader standalone cyber policies.

The key takeaway: Cyber insurance is often affordable for small businesses, but the policy form matters. A low-cost endorsement may not provide the same protection as a standalone cyber policy.

What affects cyber insurance costs the most?

When evaluating cyber insurance cost for a small business, carriers focus on several core risk factors. These eight variables help insurers assess both the likelihood of a cyber event and the potential severity of a claim.

- Industry

Some industries face higher cyber exposure because of the data they handle, the systems they rely on, or the contractual obligations they must meet.

Healthcare organizations, for example, often handle protected health information (PHI), while retailers may process payment data. Manufacturers and contractors may face business interruption risk if ransomware disrupts operations. Professional services firms may be more exposed to business email compromise, wire fraud, and confidential client data loss.

- Revenue

Revenue is one way insurers estimate potential loss severity. A larger company may experience greater business interruption losses, process more transactions, and store more customer or employee data.

A $2 million business and a $50 million business may face similar cyber threats, but the financial impact of downtime or a data breach can be very different.

- Employee count

More employees generally means more endpoints, more login credentials, and more opportunities for phishing or social engineering.

Because many cyber incidents begin with human error, insurers pay attention to how many people have access to systems and whether employees are trained to identify suspicious emails, payment requests, and account activity.

- Type of data you handle

The type and volume of data your business stores can significantly affect pricing. Businesses that collect personally identifiable information (PII), payment card data, protected health information (PHI), or sensitive client records may face more underwriting scrutiny.

These exposures can create notification costs, regulatory concerns, third-party liability, and reputational damage after an incident.

- Vendor dependence

Small businesses often rely on outside vendors for cloud hosting, payment processing, IT management, payroll, software platforms, and data storage.

If a critical vendor experiences an outage or breach, your business may still experience financial loss even if your own systems were not directly compromised. That’s why insurers often ask about vendor risk, business continuity planning, and contractual protections.

- Coverage limits and deductibles

Higher limits generally increase premiums because the insurer is taking on more potential loss. Lower deductibles, also called retentions, can also increase cost because the insurer is assuming more of the claim.

Policy type matters, too. A basic endorsement may cost less, but a standalone cyber policy may provide broader coverage for:

- Business interruption

- Data restoration

- Cyber extortion

- Privacy liability

- Incident response

- Funds transfer fraud or social engineering, depending on the policy

For a deeper explanation of what a policy may include, read our complete guide to cyber insurance.

{{richtext-cta-business-insurance="/components/rich-text-cta"}}

- Security controls

Businesses with strong cybersecurity practices are often rewarded with more favorable pricing. Multifactor authentication, software updates, and staff training, in particular, can significantly reduce both risk and cost.

If you are preparing for underwriting, our cyber insurance requirements checklist can help you understand what carriers expect.

- Claims environment

Claims trends help explain why pricing varies. Coalition’s 2026 claims data shows that business email compromise and funds transfer fraud accounted for 58% of all claims across its policyholders in 2025, while ransomware demands surged past $1 million on average—even as most businesses refused to pay.

These trends explain why insurers look beyond surface-level information. They want to understand how exposed your business is to email-based fraud, vendor disruption, and operational downtime.

For additional context, check out our article on the top cyber security threats facing small businesses.

How 2026 cyber insurance costs compare with the last decade

This conversation looks very different from what it did 10 years ago. Market estimates show global cyber premiums growing from about $3.5 billion in 2016 to an estimated $16.9 billion in 2025 and $19.6 billion in 2026.

In the U.S., the NAIC reports that total cyber direct written premiums rose from about $4.07 billion in 2020 to $9.84 billion in 2023, then declined 7.11% to $9.14 billion in 2024 as the market cooled.

That pattern tells an important story.

The cyber market hardened sharply in the early 2020s as ransomware and other losses put pressure on carriers. Today, pricing has retreated from those highs. Overall pricing is now more comparable to the beginning of the hard market cycle in the first half of 2021, largely because of carrier competition.

In other words, the market is still competitive, but it is no longer new or immature. Buyers have more options, and insurers are using better data to differentiate between high and low risks.

Where cyber insurance costs may be headed next

For many well-controlled small businesses, the near-term outlook still points to flat to slightly softer pricing—not a major jump. Still, not every business will see the same result.

Healthcare is one sector where competition is less fierce, and pricing has increased in single digits. Third-party outages, systemic vendor risk, and AI-related exposures are putting pressure on underwriters. Markets are also aggressively underwriting wrongful collection and other emerging exposures.

So while the cyber insurance cost for a small business may stay favorable for many buyers in 2026, businesses with weak controls, heavier privacy exposure, poor claims history, or higher-hazard operations may feel firmer pricing sooner than others.

Cyber insurance is also easier to justify when you compare premiums to potential loss. The average U.S. data breach cost reached a record $10.22 million in 2025. While not every incident will be that large for a small business, recovery costs can escalate quickly once you factor in forensics, notification, legal expenses, interruption, fraud loss, and reputation damage.

How to lower your cyber insurance premium

Not every factor is within your control, but strong cybersecurity practices can improve your risk profile and may help reduce your premium.

- Enable multifactor authentication (MFA)

MFA is one of the most important controls carriers look for. At a minimum, businesses should use MFA for email, administrative accounts, and remote access.

- Maintain tested backups

Backups are especially important for ransomware recovery. Insurers want to know that backups are secure, segmented, and tested regularly, not just that they exist.

- Use endpoint detection and response (EDR)

Endpoint detection and response tools help identify suspicious activity across laptops, servers, and other devices. This can reduce both the likelihood and severity of a cyber event.

- Patch critical systems quickly

Unpatched vulnerabilities remain a common entry point for attackers. Businesses should prioritize security updates for internet-facing systems and maintain an inventory of software and devices.

- Train employees on phishing and fraud

Business email compromise and funds transfer fraud remain major claim drivers. Training employees to recognize suspicious requests, verify payment changes, and report unusual activity can reduce the likelihood of a costly incident.

- Review vendor dependencies before renewal

Before renewal, identify your most critical vendors and consider how an outage, breach, or service disruption would affect your business. Strong vendor oversight can support better underwriting conversations.

- Compare standalone cyber vs. endorsement options

Endorsements added to existing policies may offer limited protection at a lower cost. Standalone cyber policies typically provide broader coverage, including business interruption, ransomware, and incident response.

While endorsements may seem more affordable upfront, they may not provide sufficient protection in a serious event. Comparing options can help you balance cost and coverage more effectively.

- Take a proactive approach to underwriting

Ultimately, lowering your cyber insurance premium is about demonstrating that your business takes cyber risk seriously. Insurers are looking for strong technical controls, clear internal processes, and awareness of evolving threats.

If you’re unsure where your organization stands, our cyber insurance requirements checklist provides a helpful overview of what carriers expect and how to prepare.

Is cyber insurance worth it for a small business?

For most small businesses, cyber insurance is worth considering because a single incident can create costs that go far beyond IT repair.

Even a relatively small incident can involve multiple cost layers, including:

- IT forensics and incident response

- Legal and regulatory compliance costs

- Customer notification and credit monitoring

- Business interruption and lost revenue

- Reputational damage

Cyber insurance is not a replacement for strong cybersecurity practices. It works best as part of a broader risk management strategy that includes employee training, vendor oversight, access controls, backups, and incident response planning.

For more perspective, read our article on the value of cyber insurance.

Get a cyber insurance quote built for your business

Cyber insurance costs can vary significantly, but so can your exposure. The best way to understand what your business actually needs is to evaluate your operations, data, vendors, contracts, controls, and coverage goals.

Christensen Group can help you:

- Identify cyber risks based on your business operations

- Review the cybersecurity controls insurers expect

- Compare coverage options across leading carriers

- Evaluate standalone cyber, endorsement, and specialty policy options

- Structure coverage that aligns with your budget and risk tolerance

Whether you are buying cyber insurance for the first time or reviewing an existing policy, our cyber insurance experts can help you make a more informed decision. And because cyber coverage should never sit in a silo, we can also help you fit it into your broader business insurance solutions strategy.

Talk with our team today to get a customized cyber insurance quote and risk assessment.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

%20(1).webp)