Max Wilber serves as Senior Vice President and Head of Alternative Risk at Christensen Group, where he oversees key partnerships and strategies involving third-party administrators, pharmacy benefit managers, stop-loss carriers, and group captive markets. With extensive experience building captive programs from the ground up, Max specializes in helping clients transition from fully insured to self-funded arrangements.

{{cta-contact-popup="/components/rich-text-cta"}}

For years, employers—especially in the mid-market space—have been stuck with limited options when it comes to funding health benefits. Fully insured plans offer predictability but at a cost: limited control, minimal transparency, and rising premiums that often feel arbitrary. Level-funded plans provide a bit more flexibility but still funnel a large portion of premium dollars toward administrative costs and insurer profits. And while self-funding offers more control, it brings volatility and risk that many employers are hesitant to shoulder alone.

This is where captive health insurance enters the picture. It's not a new concept, but it’s quickly becoming one of the most strategic tools for employers who want to regain control of their healthcare spend without taking on unnecessary risk.

What is captive health insurance?

Captive health insurance—also referred to as captive medical insurance—is a funding structure where a group of employers band together to form their own insurance company, called a group captive insurance company. Instead of sending premium dollars to a traditional insurance carrier, the members of the captive collectively fund and manage their own claims.

It’s important to note that a captive is not a health plan itself. Rather, it's the financial vehicle that funds your health plan. This approach lets you retain more of your premium dollars, gain access to detailed claims data, and make better decisions for your organization’s health benefits.

How does a health insurance captive work?

Group captive insurance companies are structured to spread risk across three layers:

- Retained Layer: Each employer pays for their own small, predictable claims—those under a specified threshold, like $25,000.

- Shared (Captive) Layer: Medium-sized claims are pooled together and shared across all members of the captive. This is typically where costs between $25,000 and $250,000 are managed.

- Stop-Loss Layer: Catastrophic claims above $250,000 are passed on to a stop-loss insurance carrier to protect all members from large financial exposure.

This three-tiered approach offers a unique blend of cost control and protection, allowing employers to capture the benefits of self-funding while insulating themselves from extreme claim volatility. When comparing captive insurance vs self insurance, it's this layered protection that makes captives a safer, more collaborative model.

{{cta-employee-benefits="/components/rich-text-cta"}}

Why traditional insurance models fall short

The appeal of traditional fully insured plans lies in their simplicity—you pay a monthly premium, and the insurance company handles the rest. But this simplicity comes at a cost:

- Limited Transparency: Employers have little to no access to the data driving their costs.

- No Incentive to Reduce Claims: Since the insurer keeps any unspent claims dollars, there’s no reward for good performance.

- Renewal Frustration: Annual premium increases can feel arbitrary and disconnected from actual claims activity.

Even level-funded options, which promise partial refunds, often still direct more than 50% of your premium toward fixed costs and insurer margins. The structure simply doesn’t allow you to take full advantage of your plan’s performance.

Health insurance captive vs self‑funded plan

When deciding between a health insurance captive and a more traditional self-funded plan, employers should consider how risk is managed and shared. A self-funded plan means the employer alone is responsible for paying claims up to a certain stop-loss threshold. While this structure can offer cost savings, it also introduces a high level of risk and volatility.

In contrast, a health insurance captive spreads the risk across multiple employers. The shared layer in a captive cushions mid-sized claims, and the group collectively benefits from positive claim performance. Additionally, captives often come with built-in support systems such as peer benchmarking, advisory councils, and access to data tools—benefits not typically found in standalone self-funded plans.

Ultimately, when evaluating captive health insurance vs self-funded plan models, the decision comes down to your appetite for risk, desire for transparency, and long-term benefit strategy.

Group medical captive advantages for employers

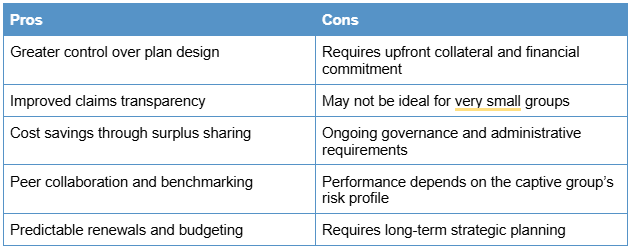

Employers exploring new ways to manage health plan costs often discover the many captive insurance advantages, including:

- Control: You choose the plan design, vendor partners, pharmacy benefit managers (PBMs), and third-party administrators (TPAs).

- Transparency: Full access to claims data helps you make smarter decisions about benefits, care management, and member engagement.

- Cost Savings: Surplus dollars that would normally go to a carrier can instead be retained or returned to captive members.

- Collaboration: Peer benchmarking, advisory councils, and shared best practices allow employers to learn from each other and optimize performance.

- Predictability: Renewal volatility is significantly reduced, making long-term financial planning more accurate and less stressful.

Here's a quick breakdown of some of the captive health insurance pros and cons:

Understanding these captive health insurance advantages and disadvantages can help employers determine if this model aligns with their long-term goals.

Who should consider a captive?

Captive medical insurance isn't for everyone, but it can be a game-changer for the right organizations. You may be a good fit if your business:

- Has between 50 and 1,000 employees

- Is financially stable and able to fund a modest amount of collateral

- Is frustrated with fully insured renewals and rising costs

- Values access to claims data and a more strategic approach to plan management

- Wants to move beyond reactive insurance renewals and into proactive health risk management

Industries like manufacturing, healthcare, construction, and transportation are especially well-positioned for captives due to their frequent exposure to high claims volatility and long-term risk management needs.

The results speak for themselves

According to a 15-year study by Berkeley Accident & Health, employers in group captives consistently outperform their fully insured peers:

- 92–93% retention rate among captive members

- 8–10% first-year savings for groups transitioning from fully insured

- 6.2% average annual renewal trend (compared to 12–15% in the open market)

- $78 million in surplus returned to members

- $226 million in collateral returned

These outcomes highlight the real-world benefits of joining a health insurance captive. As you can see, captive health insurance is not only sustainable—it’s scalable. And most importantly, it offers long-term value that far exceeds traditional insurance solutions.

Take the next step with Connect Re Captive

At Christensen Group Insurance, we believe the future of healthcare funding lies in smarter, more collaborative solutions. That’s why we created Connect Re Captive—our exclusive group captive insurance solution built specifically for mid-sized employers who are ready to take control.

With Connect Re Captive, you gain:

- Full access to claims data

- Customized stop-loss structures and plan designs

- Peer collaboration through a strategic advisory council

- Flexibility to join at any time of the year

Plus, our partners at Berkeley Accident & Health bring more than 49 successful captives and $800M in stop-loss coverage to support your success.

Ready to explore the next evolution of your employee benefits strategy? Connect with our team to schedule a complimentary funding analysis. Let’s find out if Connect Re Captive is the right fit for your business.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

%20(1).webp)